The post Steven Burke Shares Expertise on Sustainable Use of Mass Timber as a Building Material with the Washington Business Journal first appeared on Consigli Construction.

The post Steven Burke Shares Expertise on Sustainable Use of Mass Timber as a Building Material with the Washington Business Journal appeared first on Consigli Construction.

]]>Weighing in alongside other industry experts, Burke in particular emphasized the utility of mass timber as a building material, and how its use as a low embodied carbon material offers significant sustainability benefits to construction projects.

“The use of wood, and specifically mass timber, can have a considerable advantage when it comes to achieving environmental goals when the wood is harvested and utilized sustainably. Inevitably, materials sourced from our built environment like steel and concrete generate greenhouse gas emissions while they are produced, whereas the use of wood stores carbon even after the trees have been cut down. Additionally, by utilizing wood, we are able to leverage existing, naturally occurring materials in a project’s design and construction.”

Consigli has championed the use of mass timber in the industry, and its teams have coordinated and managed its use in more than fifteen projects incorporating timber solutions in design and construction. While often used in higher education, the use of mass timber continues to expand to wider-ranging, and larger-scale projects in various markets sectors.

Additionally, Consigli collaborates with research institutions, universities and testing laboratories locally and globally to continue the advancement of mass timber as a building material.

The post Steven Burke Shares Expertise on Sustainable Use of Mass Timber as a Building Material with the Washington Business Journal first appeared on Consigli Construction.

The post Steven Burke Shares Expertise on Sustainable Use of Mass Timber as a Building Material with the Washington Business Journal appeared first on Consigli Construction.

]]>The post Market Outlook: June 2021 first appeared on Consigli Construction.

The post Market Outlook: June 2021 appeared first on Consigli Construction.

]]>Market Outlook: June 2021

Peter Capone, Director of Purchasing & Jared Lachapelle, VP of Preconstruction

To access a full PDF of this information, click here: 2021 Market Outlook_06.01.21

The post Market Outlook: June 2021 first appeared on Consigli Construction.

The post Market Outlook: June 2021 appeared first on Consigli Construction.

]]>The post 2021 Market Outlook: Material and Labor Supply Update first appeared on Consigli Construction.

The post 2021 Market Outlook: Material and Labor Supply Update appeared first on Consigli Construction.

]]>2021 Market Outlook: Material and Labor Supply Update

Insight from Peter Capone, Consigli’s Director of Purchasing

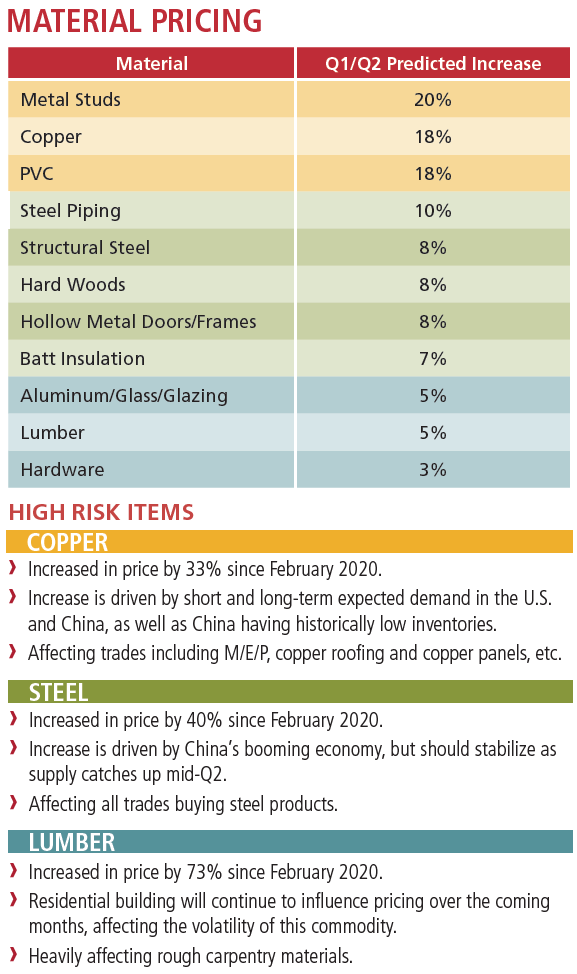

EVOLVING TRENDS

TECHNOLOGY ADVANCEMENT

TECHNOLOGY ADVANCEMENT

The pandemic has motivated subcontractors and vendors to implement technological advancements into their shop and field processes. Cost saving material management software, tool upgrades and robotics are improving efficiencies which is allowing subcontractors the flexibility in managing on-site workforce restrictions.

PRE-FABRICATION

PRE-FABRICATION

Surveyed participants are pre-fabricating 20%more than before the pandemic, assisting in managing workforce requirements in the field.

DESIGN-ASSIST

DESIGN-ASSIST

71% of our respondents noticed an increase in requests for design-assist proposals which further confirms the need for speed-to-market becoming a priority of many clients. Ensuring the construction manager has a defined process for properly implementing this approach will benefit project schedules. Vetting subcontractors for similar project experience, backlog capacity and financial wherewithal should be a focus.

WORKFORCE RESOURCES

72% of the surveyed subcontractors are not concerned with staffing projects in 2021. Based on work in the pipeline, we should continue to monitor workforce resources for 2022.

RECOMMENDATIONS

- Continue to keep a close eye on high risk materials.

- Lock in subcontractor pricing as soon as possible to avoid future price escalation.

- Hold contingencies for material escalation in estimates and budgets to avoid exposure.

- Watch for supply chain disruptions from products sourced overseas. We continue to receive delay notifications for products

such as flooring, cabinetry, etc. so we suggest procuring from domestic vendors when possible. - Identify long-lead materials and ask subcontractor and vendors about alternate materials and options.

To access a full PDF of this information, click here:

2021 Market Outlook_Material and Labor Supply Update

The post 2021 Market Outlook: Material and Labor Supply Update first appeared on Consigli Construction.

The post 2021 Market Outlook: Material and Labor Supply Update appeared first on Consigli Construction.

]]>The post COVID-19: Cost Implications first appeared on Consigli Construction.

The post COVID-19: Cost Implications appeared first on Consigli Construction.

]]>COVID-19 Cost Implications

Insight from Jared Lachapelle, Chief Estimator, Consigli

We are connecting with hundreds of subs and suppliers each week through a strong workbook of preconstruction and bidding opportunities, as well as on-going project procurement for which we are awarding 30-40 contracts per week. We expect to learn a lot in April and May and will provide updates along the way.

EXPECTATIONS

EXPECTATIONS

Our expectation is that the next few months will be turbulent, fueled by uncertainty at all levels of our industry. We therefore expect inconsistency related to cost, with some projects experiencing cost increases while others remain somewhat steady. We expect this pattern to continue as long as many construction sites and non-essential businesses are closed.

We expect stabilization relatively soon after construction broadly resumes. We expect costs to increase related to COVID-19 protocols as further described below but anticipate some or all those costs to be offset by de-escalation related to bidder aggression. We believe it unlikely that costs will rise as much as recent years where we saw as much as 7-8% escalation in some areas, comparing future costs to pre-COVID. We therefore expect, on average, to see zero to moderate per annum increases in the near-term, depending of depth and duration of a recession.

EVIDENCE OF PRICING STABILITY

EVIDENCE OF PRICING STABILITY

CURRENT PROCUREMENT

Procurement of subcontracts and materials purchases had revealed no trend change from recent awards through Friday April 3rd. The variance from budgets set by GMP’s remains typical. However, the COVID-19 safety protocols now being implemented industry wide and formalized into job specific plans have been deployed to subcontractors for inclusion in bids moving forward. We have some early impressions discussed below.

MATERIALS/EQUIPMENT PRICING

Supply chain issues do not appear to impact costs at this time, but this could change rapidly and meaningfully based on each manufacturer’s supply logistics, and whether or not and to what extent their workers and partners are directly affected by positive tests for COVID-19.

Subs and suppliers continue to consistently report minimal to no lead time impacts and no cost impacts. Most manufacturers/fabricators have reported operating at or near capacity and generally keeping up with demand. Subcontractors are consistently reporting that supply chains have been altered where needed mitigating any potential impacts. Cox Engineering CEO Jon Desmond reported in an industry roundtable hosted by Vermeulens, that supply chains are in-tact, with some Chinese supplies currently being procured elsewhere due to on-going trade tensions pre-dating COVID-19. Additionally, one manufacturer reported canceling a planned Spring price increase.

We anticipate a greater level of flexibility in material specification and selection, provided we do our part to source and present appropriate alternatives.

POTENTIAL FOR VOLATILITY

POTENTIAL FOR VOLATILITY

BIDDING BEHAVIOR

In spite of general stability at this moment, things are evolving daily, and stability could begin to erode quickly, pending further economic news, COVID-19 surge and regulations. We expect at least some near-term volatility in bidding behavior as subs/suppliers scramble to determine and implement procedure and protocols, adjust to remote working conditions, react to evolving supply chain conditions, manage cash flow and book new work reacting to stoppages and economic news.

A greater level of vigilance will be required in evaluating proposals for completeness. As subs/suppliers’ anxiety rises they may feel compelled to bid more work but may not posses the resources to do so effectively, resulting in pricing that is artificially high or low. We will continue to scrutinize proposals to ensure that no undue risk is taken.

We could begin to see discounts offered, which may present risk as it could be a sign of cash flow problems. Discounts can be attractive and may well benefit the buyer, but with some potential cost increasing forces (described below), extra care must be taken to ensure viability of the offer and offeror’s financial stability.

QUALITY OF INFORMATION

We are concerned that apparent supply stability portrayed by suppliers may be overly optimistic. We do not have direct evidence of misinformation and we believe what we are being told (directly) is sincere. However, a race to book work could lead to artificially optimistic views of manufacturing capacity and lead times, requiring additional scrutiny and further verification if possible.

SOURCES OF INCREASED COST

SOURCES OF INCREASED COST

LABOR PRODUCTIVITY HINDERED BY COVID-19 PROTOCOLS

Productivity is being impacted by working restrictions and COVID-19 protocols, though it is not yet quantifiable. Currently we are not yet seeing this translate into increased pricing for sub/supplier bids, but this may change. It is unclear to what extent productivity for individual tradespeople has been compromised in terms of output per worker-hour.

As protocols become more widely understood and implemented, we expect trade productivity loss to cause some cost increases. Some sources of productivity loss are: additional non-working time for COVID specific tool box talks and temperature testing; more frequent cleaning of elevators/hoists and similarly constrained spaces; daily cleaning of tools and equipment; staggered trade workday starts; and 6’ distancing requirements. The distance requirements will undoubtedly affect some operations more so than others. For example, many siding panels are installed with two workers closer than six feet, with alternatives in some cases not immediately obvious. For projects still in design, alternative materials and sizing may offer effective solutions. On the other hand, operations such as installing light fixtures, setting tile and painting that can be accomplished with a single worker may not be impacted. Other operations performed by crews, such as utilities, concrete forming and steel erection so far seem generally productive while maintaining proper distance.

This week, with site specific safety COVID plans in place, we’re starting to see bidders reacting with cost premiums. Albeit a small sample size, we are seeing premiums ranging from 2%-3.5%, with one outlier at 6.8%. These range across multiple trades, multiple jobs and a broad range of trade dollar values. One bidder reported a cost range resulting in 2.9-8.6%, which highlights the uncertainty and challenges with quantifying lost productivity.

In future updates we will expand on the productivity loss more precisely and report on trends with broader information.

EXTENDED SCHEDULES/GENERAL CONDITIONS

Although individual worker output is not compromised in some cases, there is an overall project-wide daily output reduction due to fewer workers on site. Many activities on site that were previously scheduled with start-to-start lags are now start-to-finish operations. This will have an impact on schedules, requiring longer days, 6- or 7-day work weeks, or longer durations, which will increase Division 01 costs for staffing and temp facilities rentals, etc.

INCREASED PROJECT REQUIREMENTS

Other Division 01 costs will increase due to sanitation, monitoring and reporting protocols, such as additional cleaning of common areas, job trailers, more frequent emptying of trash receptables, hourly cleaning of high touch surfaces, hand wash stations with warm water, sanitation/hygiene signage, additional PPE, technology to support greater remote collaboration and job office size/configuration to facilitate distancing.

SOURCES OF DECREASED COST

SOURCES OF DECREASED COST

BIDDER AGGRESSION

Work stoppages and the prospect of further project postponements and/or cancellations represent a disruption to the cost model for many trade partners. Since the financial crisis recovery, we have seen sustained growth which came with higher margins for many subs/suppliers. We expect many of them to demonstrate aggression based on fewer opportunities, or at least a near term fear of few opportunities. One open shop electrical subcontractor conveyed that what had been 150 bid invites received per week has turned into 20 / week.

We expect this to result in greater subcontractor participation and therefore competition. If this occurs it will act as a counterbalance to the forces increasing cost, but as noted above, it is not clear what the net effect will be and will depend heavily on the duration businesses and jobs are closed and the speed of subsequent economic recovery.

CURRENT EVIDENCE OF FOCUS SHIFT

While we don’t yet have direct evidence of cost reductions relating to a strategic shift from margin to volume some subs are noticeably anxious. Some have specifically referenced holes in their schedules, and we’ve seen a broad increase in post-bid follow up from subs/suppliers.

To access a full PDF of this information, click here:

Material-Cost-Update_041420

The post COVID-19: Cost Implications first appeared on Consigli Construction.

The post COVID-19: Cost Implications appeared first on Consigli Construction.

]]>The post COVID-19 Impact: Material Supply Update first appeared on Consigli Construction.

The post COVID-19 Impact: Material Supply Update appeared first on Consigli Construction.

]]>The information below provides a snap-shot of where we are currently and the outlook on how this will affect our industry.

Market Watch as COVID-19 Evolves

Insight from Peter Capone, Consigli’s Director of Purchasing

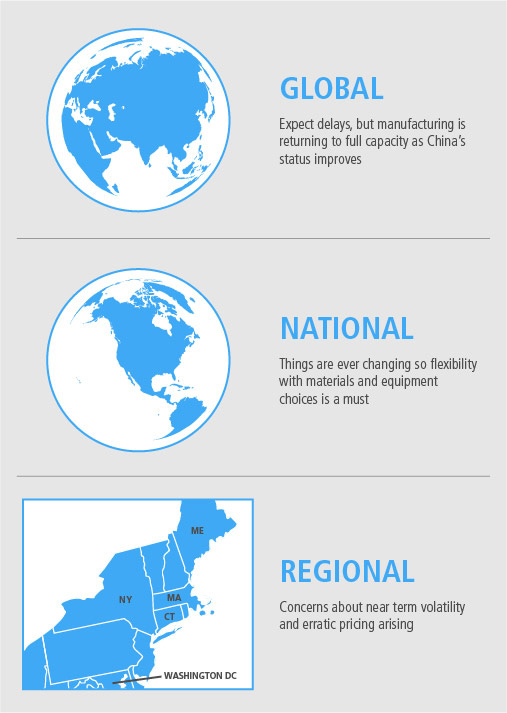

GLOBAL

GLOBAL

As time goes on, it’s becoming apparent that although we will see a lag in supply, China is in the process of recovery, therefore manufacturing has started to return to full capacity.

Constrained logistics, travel restrictions and a shortage of labor in China will most certainly cause some delay, although the slow-down in the construction industry in the United States (U.S.) will provide time for this major supplier of product to recoup.

According to a report from Construction Dive, Chief Economist for Dodge Data & Analytics Richard Branch estimated that 30% of building products in the U.S. are imported from China. While China seems to be slightly rebounding from the disease, its decreased manufacturing output is still expected to impact construction in the United States.

NATIONAL

- The differing State mandates from local governing authorities continue to make tracking the reliability of domestic supply chain a day to day challenge.

- The enforcement of mandatory protocols has caused drops in efficiencies in the manufacturing work force as well as the on-site installation work force. We expect to see these protocols become more stringent “IF” cases of the virus continue to increase. Receipt of Steel and Pre-cast Concrete from Quebec and other parts of Canada is also changing daily as fabricators apply for dispensation. Currently most fabricators are being allowed to deliver to the U.S. That being said, there is rumor that deliveries may be delayed due to driver quarantines.

- Many domestic fabricators in Pennsylvania, New York, Georgia and other states are shutting down and reducing fabrication plant activity, which will delay deliveries of millwork, aluminum windows, brick and now potentially flooring products. As the virus flows through each state, knowing where your materials are coming from, remains exceedingly important.

- Owner’s/Architects should prepare to be more flexible with material/equipment choices depending on schedule and cost risks and priorities.

- Electrical fixtures and Mechanical equipment – although parts and pieces may shortly be available, domestic fabricators will be required to assemble.

- According to analysis done by S&P Global Platt, China’s output of finished steel, a key export in American building projects, was expected to fall by up to 43 million metric tons year-over-year last month due to the Coronavirus outbreak.

- According to an article from Construction Dive on April 2, 2020:

- COVID-19 exposed inefficiencies in the way the U.S. sources materials/merchandise/etc.

- As a result there will be more focus on U.S. manufactured materials

- This could be an opportunity to look at local or U.S.-based prefabrication to cut out the international supply chain for materials

REGIONAL

Concerns are rising about near term volatility and erratic pricing as subs scramble to work from home and figure out COVID impacts.

PRECAUTIONARY MEASURES

- Consigli has maintained focus on tracking products. Domestic fabrication is now under the microscope. Communicating with Vendors and understanding “What’s left on the shelf” is of vast importance, as fabrication plants reduce output due to labor reductions.

- We’ve continued to keep a close eye on “over saturation” of Subcontractors and Vendors. Spreading the work to minimize risk while at the same time keeping as many of our partners working, has become a very high priority.

- Early buyout of high dollar, long lead-time packages has remained a priority.

- Awarding packages with an initial commitment for payment of shop drawings and design services, prior to fully committing to material procurement has lessened the risk for all parties.

To access a full PDF of this information, click here:

Material Supply Update_040720

The post COVID-19 Impact: Material Supply Update first appeared on Consigli Construction.

The post COVID-19 Impact: Material Supply Update appeared first on Consigli Construction.

]]>The post COVID-19 Impact: Construction Materials first appeared on Consigli Construction.

The post COVID-19 Impact: Construction Materials appeared first on Consigli Construction.

]]>Overview

On an ongoing basis, we continue to work closely with all our supply chain partners to better understand any current or potential impacts from COVID-19 on materials used in our projects.

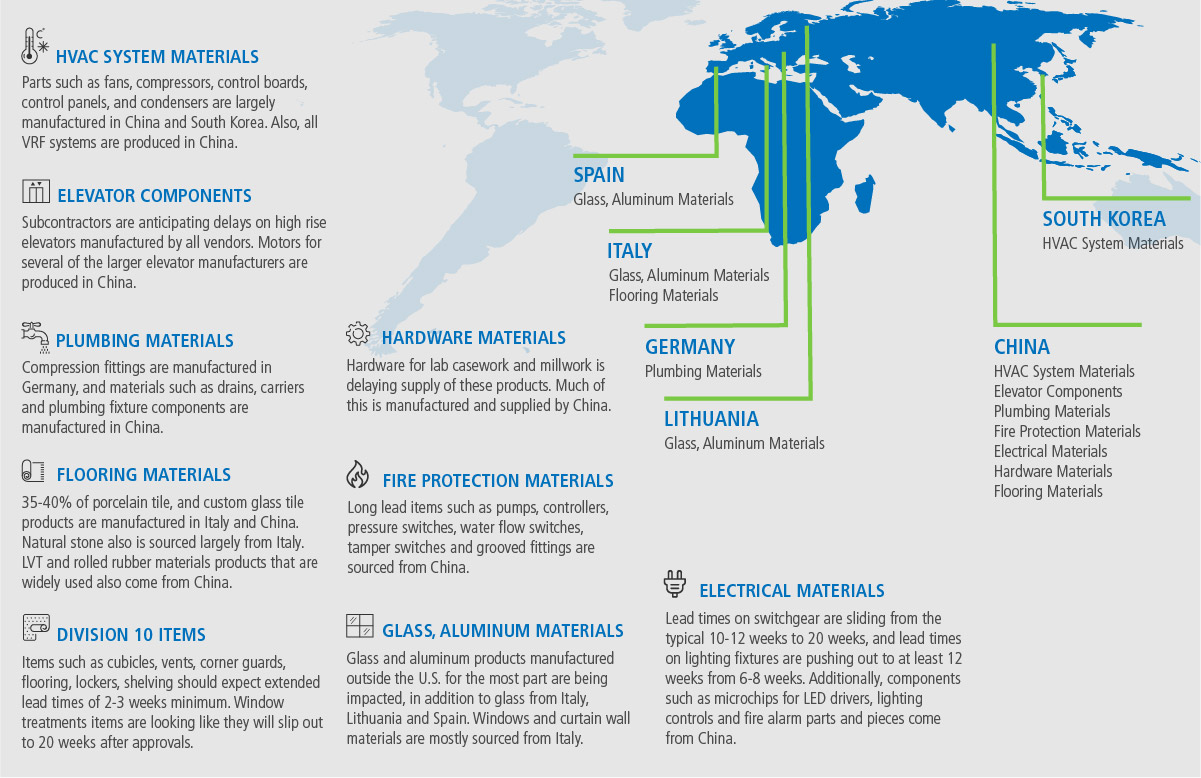

We have already seen some early signs of potential impacts to our supply chain but truthfully, it is too early to tell the broader extent of these impacts. The hardest hit countries that supply materials for our industry are: China, Italy, South Korea, Germany, Spain and France. So far, we’ve found that select components used in electrical fixtures and equipment, mechanical equipment and elevator equipment are of the largest concern due to a mix of manufacturing shutdowns and port of call export restrictions. Consigli felt it was judicious to offer insight as to how the virus has already impacted, and may continue to impact, the supply chain of materials. Consigli’s Director of Purchasing Peter Capone offers some current thoughts as to what we’re seeing in the marketplace now, and we’ll continue to monitor the situation.

Scale of Impact

GLOBAL

Over the past few weeks (and likely weeks to come), global shipping has been one of the biggest casualties. More tonnage of container ships is idled around the world now than during the global financial crisis, according to Alphaliner, a shipping data service. China’s manufacturing sector has been hampered by efforts to contain the spread of the illness, and earlier this month, the Italian prime minister instituted a nationwide lockdown. Already, some lighting fixture components sourced from China that were ordered prior to the outbreak are back ordered. There are also longer lead times on finishing materials like glass office fronts and stone coming from Italy.

NATIONAL

About 30% of building materials imported to the U.S. come from China, making the country the biggest single supplier, according to Dodge Data. U.S. contractors are already seeing the impacts of the coronavirus on supply chains for building material—from shipping delays to a need to re-source products domestically. And the country is faced with uncertainties over how long countries will be on lockdown, how crews will be impacted and whether project deadlines will have to be pushed out. The American Association of Port Authorities also announced earlier this month that first quarter cargo volumes at U.S. ports could drop 20% or more from 2019 levels because of supply chain disruptions caused by the coronavirus.

REGIONAL

Supply of materials in the Northeast mirror what we’re seeing nationally with the exception of imports from Canada; however, of materials sourced from Canada (such as structural steel and HVAC equipment) are also starting to become concerning. Newly implemented travel restrictions have not blocked the import of materials, but Canada is ramping up its precautionary measures daily which will eventually affect manufacturing output.

POTENTIAL DELAYS

- Manufacturing Shutdowns | While factories in China are continuing to come back online as the spread of the virus subsides and materials will begin to flow again, there are still issues affecting cargo movement and back up delays.

- Port of Call Export Restrictions | COVID-19 is expected to create “a longer and larger impact” on imports flowing into major U.S. container ports than previously believed due to factory shutdowns and travel restrictions in China that continue to affect production, according to the National Retail Federation (NRF). There is still a lot of uncertainty as to the longterm impact on the supply chain.

PRECAUTIONARY MEASURES

Within the last several weeks, all of our project teams have, and will continue to, take the following precautions:

- Identify project specific “long lead time/high-risk” materials sourced abroad;

- Communicate daily with subcontractors to track these materials as they move through the process;

- Discuss contingency plans for sourcing “alternate” manufacturers, when prudent;

- Work with design teams, during design development, to avoid sourcing materials from high-risk manufacturers;

- Collect and share information daily through a centralized tracking portal;

- Expedite remaining buyout to avoid domestic material demand issues.

LOOKING AHEAD

To continue moving projects along both on time and safely, Consigli recommends teams evaluate their contracts and communicate with all project teams, subcontractors and vendors. Consigli is also now looking at sourcing materials earlier than it normally would and possibly looking to rely more heavily on domestic suppliers. More positively, we are seeing that Chinese manufacturers are back online and slowly returning to full capacity. We anticipate a portion of these potential supply delays will resolve in the coming weeks, and we will maintain open communication in the coming weeks as supply logistics play out and circumstances evolve. Stay safe and healthy, and rest assured we are all in this together.

To access a full PDF of this information, click here:

COVID-19 Impact to Construction

The post COVID-19 Impact: Construction Materials first appeared on Consigli Construction.

The post COVID-19 Impact: Construction Materials appeared first on Consigli Construction.

]]>